Malaysia’s Upcoming Carbon Tax in 2026: Boon or Bane?

Oct 21,2025

Oct 21,2025

Introduction to Carbon Tax

In Malaysia’s Budget 2026, the government officially announced the introduction of a carbon tax targeting three major sectors: energy, iron, and steel. This marks a significant milestone in Malaysia’s sustainability journey and demonstrates the government’s firm commitment to achieving its net-zero emissions goal by 2050.

The introduction of a carbon tax reflects a growing recognition that economic growth and environmental stewardship must go hand in hand. By putting a price on carbon, the government is creating a financial incentive for industries to invest in cleaner technologies, enhance efficiency, and rethink their production methods. Ultimately, this will not only reduce emissions but also help companies minimize operational costs associated with carbon liabilities and energy consumption.

Pros and Cons of Carbon Tax

At its core, a carbon tax is a price placed on greenhouse gas (GHG) emissions, typically measured in tonnes of CO₂ equivalent (tCO₂e). The more emissions a company produces, the higher the tax it must pay. Since GHGs are a key driver of global warming and climate change, taxing them creates a direct economic reason to decarbonize.

The benefits of a carbon tax are twofold:

- Encouraging low-carbon choices – When emissions come with a cost, industries are more likely to improve energy efficiency, adopt renewable energy, or switch to cleaner fuels.

- Generating fiscal revenue – The government can reinvest carbon tax revenue into renewable energy projects, green technology development, public transportation, and transition support for affected industries.

However, carbon tax implementation is not without drawbacks. Increasing the cost of carbon-intensive activities, especially in the energy and manufacturing sectors, can lead to higher production costs. These costs are often passed down to consumers through higher prices for electricity, fuel, construction materials, and everyday goods. For instance, if the cost of steel rises, construction and property prices are also likely to increase. The challenge, therefore, lies in balancing environmental responsibility with economic stability.

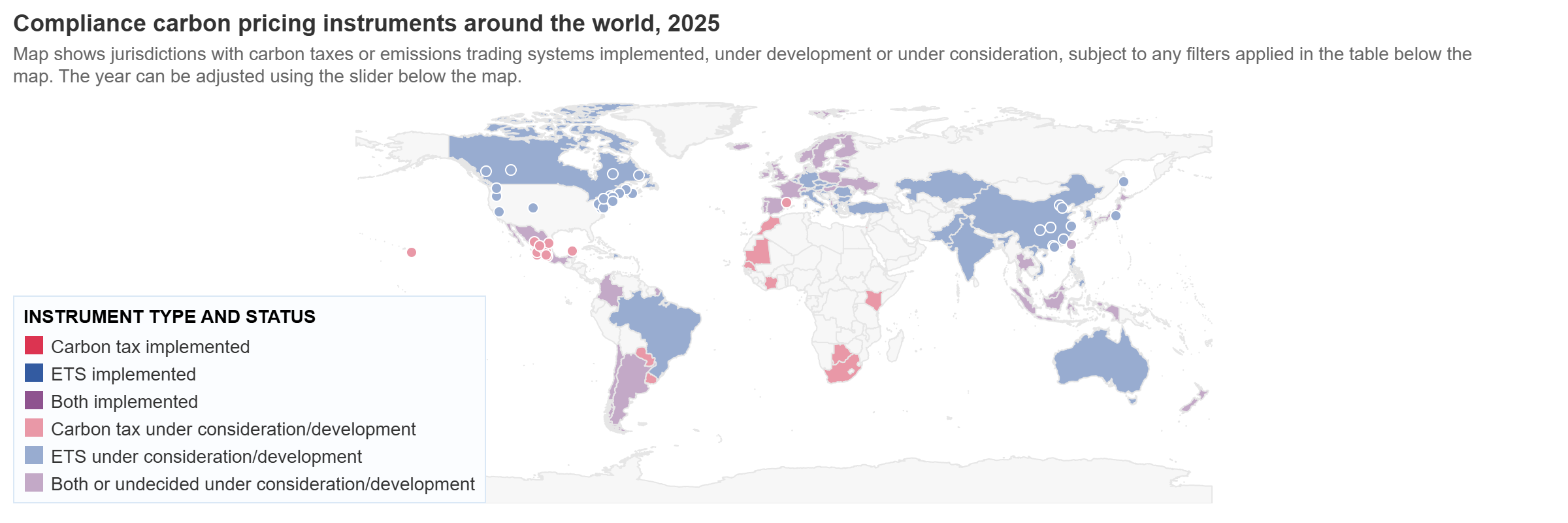

Carbon Tax Implementation Around the World

Carbon tax is not new on the global stage. It is the most widely adopted carbon pricing mechanism for reducing emissions, followed closely by the Emission Trading System (ETS). To date, over 43 countries have implemented some form of carbon tax, including Sweden, Switzerland, Canada, and closer to home, Singapore.

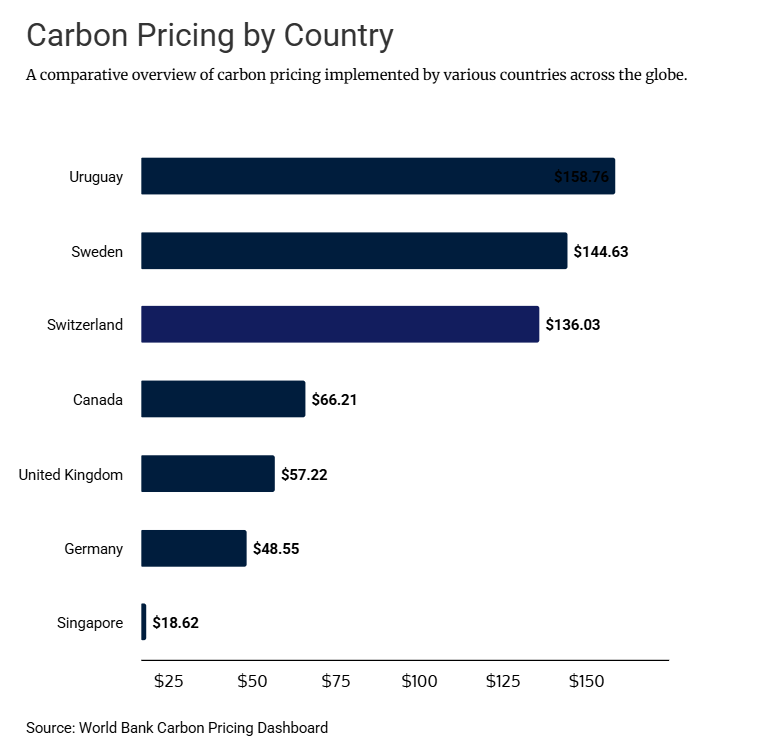

Finland and Poland were the pioneers, introducing carbon taxes in 1990. Other Scandinavian nations—Sweden, Norway, and Denmark soon followed. These countries now host some of the world’s highest carbon tax rates, exceeding US$100 per tonne of CO₂e. Developed economies generally fall in the range of US$20–70 per tonne, while developing countries, reflecting economic realities, often start below US$10 per tonne.

According to the World Bank’s Carbon Pricing Dashboard, carbon tax rates vary widely, from as low as US$0.1/tCO₂e to as high as US$158.8/tCO₂e, depending on the country’s economic structure, policy goals, and energy mix. The global trend, however, is moving toward higher prices to accelerate climate action.

Carbon Pricing Implementation in ASEAN

Malaysia’s forthcoming carbon tax will likely take inspiration from its regional peers, Singapore and Indonesia, both of which have implemented carbon pricing policies tailored to their economies.

Singapore was the first ASEAN country to introduce a carbon tax, starting in 2019 at S$5 per tonne of CO₂e. The rate has since increased to S$25 per tonne in 2024 and will rise to S$45 in 2026–2027, and S$50–80 by 2030. The Singapore model covers about 80 percent of the country’s total GHG emissions and applies to large industrial facilities emitting more than 25,000 tCO₂e per year. Revenue collected is reinvested in green transition programs and industrial innovation funds.

Indonesia, on the other hand, has opted for a hybrid system that combines an emission trading scheme (ETS) with a carbon tax component. Its carbon tax, introduced under Law No. 7/2021, started at IDR 30 per kilogram of CO₂e (roughly US$2 per tonne) and applies initially to the power sector. As its carbon market develops, Indonesia plans to expand coverage to other industries, gradually aligning tax levels with market prices.

Probable Carbon Tax Implementation Scenario in Malaysia

To gauge Malaysia’s possible direction, it is useful to look at how Singapore’s system operates. About 80 percent of Singapore’s total emissions are subject to carbon-related pricing, including fuel excise duties and carbon tax. Facilities emitting 25,000 tCO₂e or more annually are taxed, and every S$5/tCO₂e increase in carbon tax roughly raises electricity tariffs by 1 percent. The tax applies to major emitters in the manufacturing, power, waste, and water sectors. Starting in 2024, Singapore also allows companies to use high-quality international carbon credits (ICCs) to offset up to 5% of their taxable emissions, encouraging flexibility while maintaining environmental integrity.

Malaysia’s emissions profile, according to the International Energy Agency (IEA), shows that electricity and heat producers account for 49 percent of national CO₂ emissions, followed by transportation (22 percent) and industry (15 percent). This aligns closely with the Budget 2026 announcement, which targets the energy, iron, and steel sectors; industries dominated by large players that can be more easily monitored and taxed.

Interestingly, cement production and transportation sector, another 2 major emitters, were not included in the initial list. The exclusion could be temporary, as the sectors may be brought into the framework in later phases once mechanisms are established.

As industries await further clarity, one key question remains: what will be the emission threshold for tax liability? If Malaysia adopts a similar benchmark to Singapore’s 25,000 tCO₂e threshold, many medium to large facilities could fall within the taxable range. For context, burning approximately 9,300 liters of diesel annually already generates around 25,000 tCO₂e. To help visualize this, 9,300 liters per day translates to about 775 liters of diesel per month, which is only 2.5 times higher than the recently announced subsidized petrol allowance of 300 liters per month.

In terms of pricing, analysts expect Malaysia’s carbon tax to start between RM10 and RM75 per tonne of CO₂e, positioned between Indonesia’s low initial rate and Singapore’s more ambitious levels. However, most experts predict a starting rate of below RM25 per tonne to ensure a smooth rollout and avoid inflationary pressure.

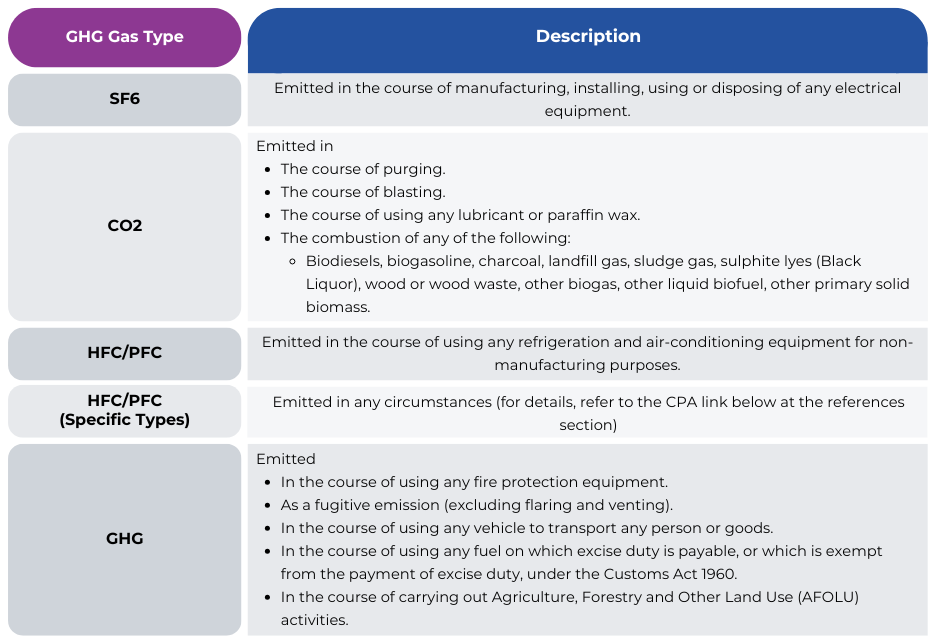

Finally, it is interesting to investigate on the types of GHG emissions that are taxable under Singapore Carbon Pricing Act. According to the Act, all reckonable emissions are eligible for tax, and reckonable emissions means any GHG emission other than a non-reckonable GHG emission. The list of non-reckonable emissions is as below:

Based on the table, it can be concluded that most Scope 1 emissions, including stationary combustion, mobile emissions, process emissions, and fugitive emissions are taxable, with one key exception. Fugitive emissions arising from the unintentional release of HFCs or PFCs due to refrigeration and air-conditioning activities are not taxable under the Carbon Pricing Act (CPA).

Interestingly, while CO₂ emissions from the combustion of biomass fuels such as biogas, biodiesel, or other solid biomass are exempt from tax, other greenhouse gases generated during the same process, such as N₂O and CH₄, remain taxable.

On the other hand, Scope 2 emissions from purchased electricity are not taxed under the CPA, as the excise duty has already been imposed on the fuels used for power generation. Similarly, emissions generated from the use of vehicles to transport people or goods are excluded since the fuel consumption (petrol, diesel, biodiesel) has already been taxed under Scope 1 mobile emissions.

In summary, the CPA focuses only on direct emissions that are within a facility’s operational control (Scope 1). Scope 2 purchased electricity is taxed at the generation stage, e.g., by TNB in Peninsular Malaysia and therefore is not subject to an additional carbon tax at the user level.

Looking Ahead

The carbon tax introduction in 2026 marks a defining moment in Malaysia’s transition to a low-carbon economy. More than a fiscal instrument, it symbolizes a structural change in how the country integrates sustainability into economic planning. It is also double edge-sword

To ensure success, the policy must be transparent, predictable, and equitable. The government will need to clearly communicate how rates are set, how revenues will be used, and how exemptions or thresholds will be managed. Complementary measures such as expanding renewable energy capacity, improving energy efficiency, and strengthening emissions data systems will be essential to reinforce the tax’s impact.

Carbon tax can be a boon if well designed, driving green innovation, attracting sustainable investments, and enhancing Malaysia’s international competitiveness. But it can also be a bane if poorly executed, leading to inflationary pressure and industrial pushback. The difference will depend on how effectively the government balances ambition with practicality.

If implemented thoughtfully, Malaysia’s carbon tax could become a cornerstone of the nation’s sustainability strategy, aligning economic growth with climate responsibility and positioning Malaysia as a credible player in the global low-carbon transition.

References:

CreativeFlow

8 month agoBookmarked for future inspiration!